As we move further into spring, the broader U.S. economy continues to send mixed signals. Inflation remains stubbornly above target, keeping pressure on the Federal Reserve as it holds rates steady, while a slight uptick in jobless claims and a cooling jobs report suggest the labor market may be losing some momentum. At the same time, consumer spending is still holding up, though largely driven by higher prices rather than real growth. In this month’s update, we’ll break down these key headlines and what they could mean for interest rates, housing activity, and the market outlook in the months ahead.

Headlines

March Jobs Report - U.S. jobless claims unexpectedly dropped to 202,000, signaling low layoffs and a stable labor market despite slow hiring, while continuing claims rose to 1.84 million, indicating some workers are taking longer to find jobs. However, economic uncertainty is increasing due to the ongoing Middle East conflict, which has driven oil prices up over 50%, pushed gas prices above $4 per gallon, and contributed to a $3.2 trillion stock market loss. These factors could reduce consumer spending, raise business costs, and weaken future hiring. At the same time, trade deficits widened and GDP growth forecasts were slightly lowered, reflecting broader economic pressure from tariffs, global instability, and slowing job growth.

Weekly Jobless Claims - In the week ending April 4, U.S. initial jobless claims rose to 219,000, an increase of 16,000 from the prior week’s revised level of 203,000, while the four-week moving average edged up to 209,500, signaling a slight but steady increase in claims without indicating major labor market weakness. Despite this uptick, overall conditions remain relatively stable, supported by low continuing claims and consistent hiring trends, though inflation and global uncertainties continue to weigh on the broader economic outlook. At the state level, Utah showed a more noticeable increase, with claims rising by 304 to 1,646 from 1,342 the previous week, suggesting some localized softening even as national data points to a still-resilient labor market.

Consumer Price Index - U.S. inflation surged in March, driven largely by a sharp spike in fuel costs linked to the ongoing conflict with Iran, with the Consumer Price Index rising 0.9% for the month, the biggest increase since mid-2022 and 3.3% year-over-year. Gasoline prices alone jumped over 21%, accounting for nearly three-quarters of the increase, while diesel and other fuel costs also saw record gains, pushing overall living expenses higher. Although core inflation (excluding food and energy) rose more moderately, economists warn that the full impact of rising oil prices has yet to be felt and could lead to broader price increases in the coming months, affecting transportation, goods, and consumer spending, while also reducing the likelihood of interest rate cuts this year.

Fed Meeting - In March, the Federal Reserve decided to keep interest rates steady at 3.5%–3.75% as it navigates a complex economic environment marked by higher-than-expected inflation, mixed labor market signals, and uncertainty from the ongoing Iran war. While the Fed still expects possible rate cuts in the future, rising oil prices and inflation concerns, partly driven by the conflict, have made policymakers more cautious. Economic growth projections were slightly increased, but inflation is now expected to remain elevated before gradually returning to target levels, and unemployment is projected to stay around 4.4%. Overall, the Fed is taking a wait-and-see approach due to global instability, political pressure, and unclear economic impacts from the war.

HUD Withdraws Fair Housing Guidance: A Turning Point for Housing Compliance

The U.S. Department of Housing and Urban Development (HUD) has taken a significant step in reshaping the federal fair housing landscape. On April 6, 2026, HUD finalized the withdrawal of multiple guidance documents issued by its Office of Fair Housing and Equal Opportunity (FHEO), formalizing an earlier action that became effective on September 17, 2025.

While this move does not change the Fair Housing Act (FHA) itself, it marks a fundamental shift in how fair housing compliance is interpreted, enforced, and operationalized across the rental housing industry.

A Shift Away from Interpretive Guidance

The withdrawn documents, some dating back more than a decade, served as interpretive frameworks that helped housing providers understand how HUD applied the law in practice. These included guidance on:

Reasonable accommodations, including emotional support animals

Criminal history screening in tenant selection

National origin discrimination and Limited English Proficiency (LEP)

Digital advertising practices

Source of income protections and testing

Special purpose credit programs

HUD clarified that these materials were non-binding policy statements, not formal regulations. However, they had become deeply embedded in compliance strategies across the industry.

With their removal, HUD has signaled that these interpretations will no longer guide enforcement decisions—either internally or externally.

The Policy Context: Deregulation and Federal Direction

This action is part of a broader deregulatory agenda under the Trump administration, aligned with:

Executive Order 14192: Unleashing Prosperity Through Deregulation

Executive Order 14219: Ensuring Lawful Governance and Implementing the Department of Government Efficiency Initiative

Together, these initiatives emphasize reducing reliance on sub-regulatory guidance and focusing federal enforcement on the statutory text of the law.

The National Apartment Association (NAA) has supported aspects of this shift, advocating for simplified compliance frameworks that reduce administrative burden while maintaining fair housing protections.

What Changed

HUD’s withdrawal eliminates its official interpretations of how the FHA should be applied in specific scenarios. As a result:

Housing providers no longer have HUD-endorsed benchmarks for evaluating fair housing issues

Compliance strategies must now rely more heavily on statutory language and court rulings

Enforcement is expected to focus more narrowly on clear violations and intentional discrimination

This creates greater flexibility—but also introduces uncertainty.

What Did Not Change

Despite the withdrawal, the legal foundation remains intact:

The Fair Housing Act is unchanged

Protections against discrimination based on race, color, religion, sex, familial status, national origin, and disability remain fully enforceable

Requirements to provide reasonable accommodations still apply

Additionally, HUD’s action does not override state or local laws, many of which impose stricter or more detailed obligations than federal standards.

A New Enforcement Environment

HUD’s current approach reflects a broader philosophy of regulatory restraint. Enforcement is likely to rely more on:

Clear statutory violations

Judicial interpretation rather than agency guidance

Case-by-case analysis across jurisdictions

This may lead to increased variability in how fair housing issues are evaluated and resolved.

Importantly, the absence of guidance does not eliminate enforcement risk. Complaints can still be filed with HUD, pursued through state agencies, or litigated privately. Courts remain independent and are not bound by HUD’s current enforcement posture.

HUD’s withdrawal of guidance changes how fair housing rules are interpreted but not the rules themselves. The Fair Housing Act remains fully in effect, and all core obligations still apply. With fewer federal guidelines, there may be more variation in how situations are evaluated, but the key takeaway is clear: the law remains the same, even if the guidance around it has changed.

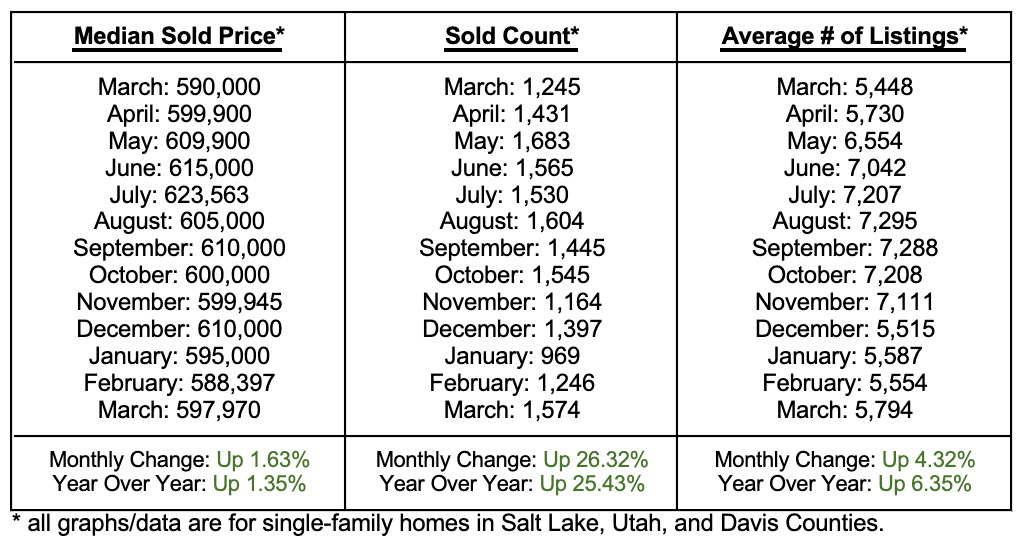

Utah Real Estate Market

Utah’s housing market gained momentum in March, signaling the start of a more active spring season. The median sold price rose to $597,970, up 1.63% from February and 1.35% year over year, showing continued price stability with slight upward movement. Sales activity saw a significant increase up 26.32% month-over-month, indicating renewed buyer demand. Inventory also increased 4.32% from February, giving buyers more options. Overall, March reflects a healthy and accelerating market, with rising sales and stable pricing, but a growing inventory could keep prices from climbing much higher.

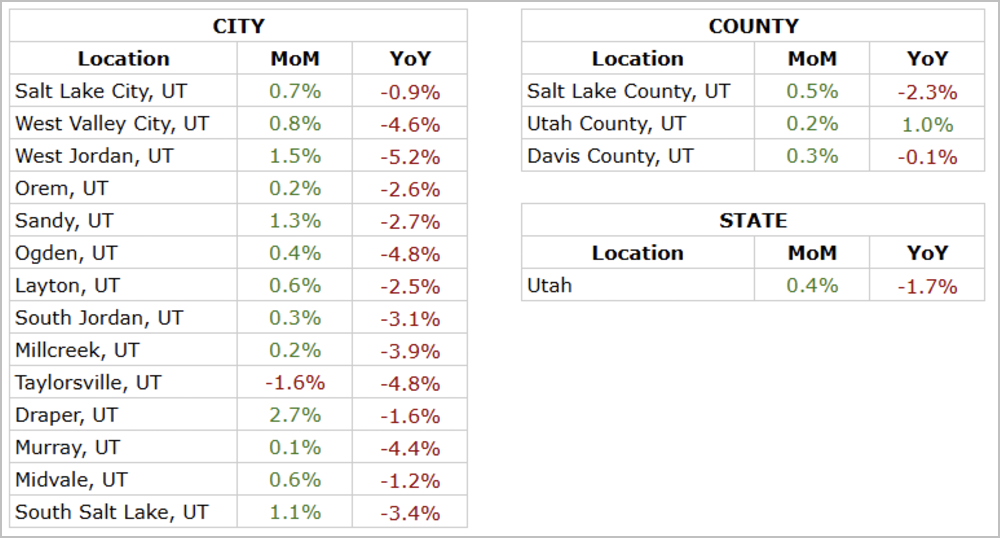

Rent Report

Utah’s rental market continued to show gradual stabilization in March, with statewide rents increasing 0.4% month over month while remaining 1.7% below last year’s levels. At the county level, Salt Lake County posted a modest monthly gain but continues to trend downward year over year, Utah County remains the strongest performer with positive annual growth, and Davis County saw slight monthly improvement with minimal annual decline. City-level trends were mixed but generally steady, with most areas experiencing small month-over-month increases led by Draper, West Jordan, and Sandy while a few locations such as Taylorsville saw minor declines. Overall, March reflects a stable rental market with modest upward movement, as conditions continue to rebalance heading into the spring season.

*Rental data provided by apartment list.

Industry Updates

Accidental Landlords Rise To Three-Year High - A growing number of homeowners are becoming “accidental landlords,” choosing to rent out their properties instead of selling in a slower housing market. According to Zillow, about 2.3% of rental listings were recently for sale, near a record high, with the trend most prominent in markets like Texas, Florida, and cities such as Denver and Nashville. This shift reflects changing market conditions where homes are taking longer to sell and sellers prefer renting over lowering prices significantly. Most of these properties are single-family homes, and the trend suggests that homeowners are not under financial distress but are instead using rentals as a strategy to wait for better selling conditions.

Single-Family Rental Yields Tighten - ATTOM’s 2026 Single-Family Rental Market report shows that while rents continue to rise in many areas, rental returns are declining in most U.S. counties due to record-high home prices increasing acquisition costs. About 54.8% of counties saw decreasing rental yields, even though rents grew faster than home prices in over half of the markets. This indicates that rising property values are compressing investor returns, making it more important to be selective when choosing markets. The strongest rental yields are concentrated in Midwestern counties, while high-cost areas like California and parts of Florida show the lowest returns. Overall, the report highlights a tightening investment landscape where rent growth alone is no longer enough to offset elevated home prices.

Summarize this content with AI:

Chat GPTGrok

Perplexity

Claude.ai