As we head into spring, the broader U.S. economy is sending mixed signals. Rising energy prices are spiking inflationary fears while a softer than expected jobs report points to potential weakness in the labor market, leaving the Fed unclear on which lever to pull when it comes to interest rates. In this month’s update, we will dive into these headlines and their potential impact on housing, plus update you on everything that happened now that the most recent legislative session has come to a close.

Headlines

February Jobs Report - U.S. employment declined in February, with nonfarm payrolls falling by 92,000 and the unemployment rate rising to 4.4%. Job losses occurred across several sectors, including health care, manufacturing, construction, and transportation. A major health care strike and severe winter weather contributed to the decline, making February marked one of several recent months with job declines. Despite weaker hiring, wages increased more than expected, rising 0.4% for the month and 3.8% year over year. While the broader economy continues to show signs of growth, the softer labor market has increased expectations that the Federal Reserve may begin cutting interest rates later this year.

Weekly Jobless Claims - U.S. jobless claims remained low last week, signaling continued stability in the labor market. Initial claims for unemployment benefits fell by 1,000 to 213,000 for the week ending March 7, remaining within the typical range seen this year and indicating that layoffs continue to stay limited. Meanwhile, continuing claims declined by 21,000 to 1.85 million, suggesting that some unemployed workers are either finding new jobs or exhausting their benefits. Despite a recent decline in nonfarm payrolls in February, economists believe the low level of layoffs indicates the labor market remains relatively resilient overall. At the state level, Utah reported 1,686 initial unemployment claims, up from 1,413 the previous week, an increase of 273 claims. While the week-to-week increase shows a short-term rise in filings, Utah’s claims remain relatively low compared to historical levels and generally reflect the broader national trend of a stable labor market with limited layoffs.

Consumer Price Index - Consumer prices rose 0.3% in February, bringing the annual inflation rate to 2.4%. This figure was in line with analyst expectations, while core inflation reached 2.5% year over year, indicating that price pressures remain slightly above the Federal Reserve’s 2% target but are holding. Housing costs increased modestly, with rent rising just 0.1%. Economists note that recent increases in oil prices could push inflation higher in the coming months, and for now, the markets expect the Federal Reserve to keep interest rates steady in the near term while monitoring economic conditions.

Fed Meeting - Since the next Federal Reserve meeting is scheduled for March 17–18, and will occur after this month’s update, we will have a quick recap of the Fed’s most recent decision. We’ll cover the outcome of the March meeting in next month’s report. At the January meeting, the Federal Reserve held its benchmark interest rate steady at 3.5%–3.75%, pausing after three consecutive rate cuts in late 2025. Officials pointed to continued economic growth, relatively stable unemployment, and inflation still hovering around 3% as reasons to take a step back and evaluate conditions before making further changes. While two governors supported another rate cut, the majority preferred to hold rates steady and continue monitoring economic data. For now, the Fed is signaling a cautious and data-driven approach, watching closely how inflation and the labor market evolve. Market expectations currently suggest the Fed may wait until mid-year before making another adjustment, depending on how economic conditions develop in the coming months.

Legislative Update: Utah Housing & Property Management Bills

The 2026 Utah Legislative Session concluded on March 6, after a 45-day legislative period in which lawmakers considered several housing-related proposals affecting rental housing providers, property managers, and tenants.

While many housing bills were introduced during the session, only a few resulted in major legislative outcomes for the rental housing industry. Below is a summary of the most significant developments.

Key Legislation That Passed

HB 377 – Real Estate Amendments (Property Management Licensing)

One of the most significant housing-related bills to pass this session was HB 377, which addresses property management licensing in Utah.

The bill provides additional time and guidance to the Utah Division of Real Estate as it works toward establishing a new “Property Management Only” license. This license would be separate from the traditional Real Estate Sales license, recognizing that many professionals manage rental properties without participating in real estate sales transactions.

The Division of Real Estate will now work through the end of 2026 to develop rules and regulations for this new licensing category.

Housing Stability Funding Approved

Despite a challenging year for state appropriations, the legislature approved funding for two housing-related programs:

- $450,000 for the Section 8 Guarantee Fund

- $450,000 for the Community Action Eviction Prevention Fund

These programs help tenants address outstanding balances and may assist in preventing evictions, which can also benefit property owners by reducing unpaid rent and turnover costs.

Major Proposals That Did Not Pass

SB 97 – Tax Revenue Amendments

One of the most closely watched bills for rental housing providers was SB 97, which proposed changes that could have increased property taxes on rental properties.

The bill ultimately failed in a close vote during the final week of the session.

For rental housing providers and property owners, this outcome means that existing property tax structures for rental properties remain unchanged for now.

Other Housing Bills That Did Not Advance

Additional proposals introduced during the session addressed topics such as:

- Tenant credit reporting initiatives, which would have required landlords to offer tenants the option to report rent payments to credit agencies.

- Pricing transparency and consumer protection requirements for housing-related services.

- Updates to residential rental statutes and landlord-tenant operational rules.

- Regulation of single-family rental properties.

- Communication requirements between landlords and tenants.

- Expanded health and safety standards for rental housing.

While many of these proposals did not advance during the 2026 session, they reflect ongoing policy discussions surrounding tenant protections, transparency in rental pricing, and regulatory oversight of rental housing operations.

Utah Real Estate Market

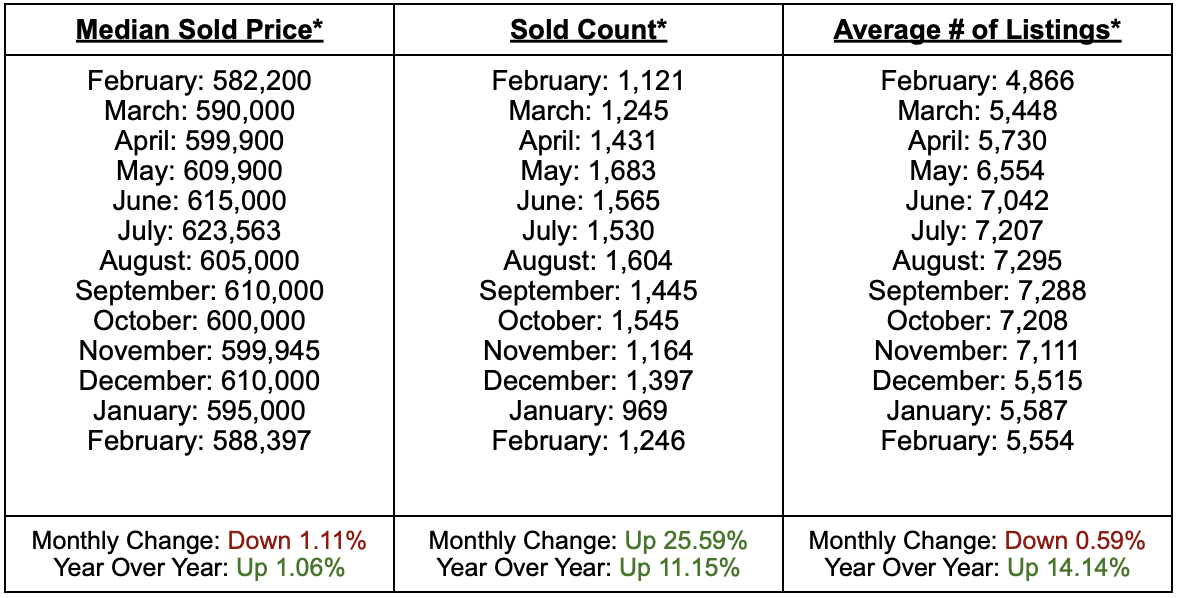

Utah’s housing market continued to show steady activity in February, with a mix of small price adjustments and growing inventory. The median sold price came in at $588,397, slightly lower than January but still about 1.06% higher than this time last year, indicating that home values remain relatively stable overall. Sales activity also improved, with 1,246 homes sold in February, up from January and over 11% higher than a year ago, suggesting buyers are becoming more active as the market transitions out of the winter slowdown. Inventory levels also remained elevated compared to last year. Active listings totaled 5,554 homes, slightly lower than January but 14.14% higher than the same time last year, providing buyers with more options. Overall, February reflects a balanced and gradually improving market, where steady pricing, rising sales activity, and expanding inventory are setting the stage for a more active spring homebuying season.

* all graphs/data are for single-family homes in Salt Lake, Utah, and Davis Counties.

Rent Report

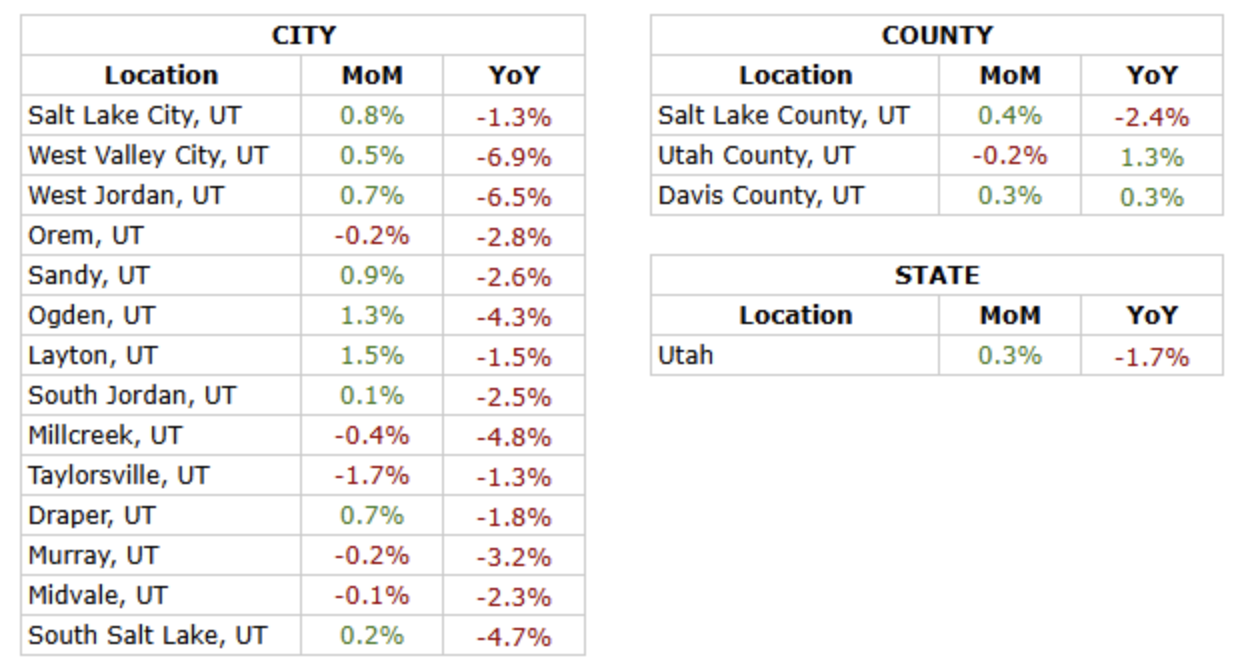

Utah’s rental market showed modest stabilization this month, with statewide rents increasing 0.3% month over month while remaining 1.7% below last year’s levels. At the county level, Salt Lake County posted a small monthly gain but remains down year over year, Utah County continues to lead with positive annual growth, and Davis County recorded slight increases both monthly and annually. City trends were mixed but generally steady. Several cities including Layton, Ogden, Sandy, and Salt Lake City saw small monthly increases, while a few areas such as Taylorsville and Millcreek experienced minor declines. Overall, the data suggests a stable rental environment with modest monthly movement as the market continues to rebalance.

*Rental data provided by apartment list.

Industry Updates

White House Targets Institutional Investment in Single-Family - The White House recently issued an executive order addressing institutional investment in single-family housing, with the stated goal of preserving housing availability for individual homebuyers. The order directs federal agencies to review policies that may enable large institutional investors to acquire single-family homes that might otherwise be purchased by owner-occupants. The order also calls for federal agencies and regulators to review large investor acquisitions and potential anti-competitive practices in single-family rental markets. In addition, certain housing providers participating in federal housing programs may be required to disclose ownership structures to help identify involvement from large institutional investors. Properties developed specifically as build-to-rent communities are expected to remain exempt from these restrictions.The administration has also directed staff to develop legislative recommendations that could formalize these policies through Congress. Industry organizations have emphasized that addressing housing supply and affordability will likely require coordination across both the rental housing and homeownership sectors.

HUD, USDA Revoke 30-Day Notice Rules - The U.S. Department of Housing and Urban Development (HUD) and the U.S. Department of Agriculture (USDA) have removed the federal requirement that housing providers give a 30-day notice before terminating a lease for nonpayment of rent in certain federally assisted housing programs. HUD’s rule will take effect March 30, 2026, while USDA implemented a similar change immediately on February 25, 2026. HUD also rescinded several pandemic-era policies that had been introduced during the COVID-19 emergency. The 30-day notice rule was originally created to allow tenants additional time to access Emergency Rental Assistance during the pandemic. With the new change, notice requirements will generally return to pre-2021 standards, which rely more on existing program rules and state or local eviction laws. Housing providers are advised to review local regulations and consult legal guidance when adjusting their procedures.

Summarize this content with AI:

Chat GPTGrok

Perplexity

Claude.ai