As we move further into the second quarter, our world is filled with mixed signals. Inflation remains elevated but has not increased as dramatically as some experts feared, the labor market is surprisingly resilient despite signs of weakness, and the stock market is hitting all time highs despite no long term resolution to the war in Iran. Meanwhile, the local rental rental market is heating up after a sluggish start to the year and sales activity is surprisingly strong despite elevated interest rates. In this month’s update, we’ll take a closer look at what’s happening both nationally and here in Utah and see what those trends might mean for your rental.

Headlines

April Jobs Report - The U.S. economy added 115,000 jobs in April, which was better than expected, while the unemployment rate stayed steady at 4.3%. Even though the overall numbers were stronger than forecasted, the report still showed signs that the job market is slowly cooling down. Wage growth slowed, fewer people were actively working or looking for work, and tech-related jobs continued to decline, partly due to companies using more AI. Healthcare, transportation, retail, and social assistance added the most jobs during the month. Overall, the labor market remains stable, but hiring is not as strong as it was in previous years, which is one reason the Federal Reserve is expected to keep interest rates unchanged for now.

Weekly Jobless Claims - U.S. unemployment claims rose slightly last week, but layoffs remain historically low, signaling that the labor market is still stable despite economic uncertainty tied to the ongoing Iran conflict and rising oil prices. Initial jobless claims increased to 200,000, remaining below levels typically associated with labor market weakness. Strong employment conditions and steady hiring continue to reduce expectations that the Federal Reserve will cut interest rates this year, especially as inflation concerns remain elevated. While some large technology companies continue announcing layoffs tied to AI adoption, overall job cuts are down significantly compared to last year. Economists expect job growth to slow in April but still remain healthy enough to support a stable labor market overall. In Utah, unemployment claims also remained stable, with advance claims declining from 1,394 to 1,328 last week, reflecting continued resilience in the state’s labor market despite broader economic uncertainty.

Consumer Price Index - The April CPI report is set to come out on May 12, so that report didn’t quite make it into this publication. We’ll include a full update and breakdown in the next report once the data is available. In the meantime, looking back at March, inflation jumped 0.9% month over month and 3.3% year over year, largely driven by a spike in fuel costs tied to the Iran conflict. Gas prices surged over 21%, accounting for most of the increase. While core inflation remained more stable, rising energy costs may continue pushing prices up and could delay potential interest rate cuts.

Fed Meeting - The Federal Reserve held interest rates steady at 3.5%–3.75% in its latest meeting, but the decision revealed an unusually divided stance among policymakers, with an 8–4 split—the highest level of dissent since 1992. Officials are balancing persistent inflation, driven in part by rising energy prices, against signs of a softening but still stable labor market. While some members pushed for rate cuts, others opposed signaling any easing due to concerns that inflation remains elevated above the Fed’s 2% target. Markets currently expect little to no rate changes in the near term, reflecting ongoing economic uncertainty. This meeting also marked a potential leadership transition, with Chair Jerome Powell expected to step down soon, adding another layer of uncertainty to future policy direction.

Utah Housing Market: Short-Term Pressure, Long-Term Opportunity for Rental Owners

The U.S. rental market in 2026 has shifted into a more renter-friendly environment, largely driven by a wave of new housing supply entering the market. This has led to rising vacancy rates, slower rent growth, and increased competition among landlords.

However, this current condition is only part of the story.

Across the country, builders are beginning to pull back on new construction due to high interest rates, rising material costs, and softer demand. This slowdown signals a shift in future supply when fewer projects are started today, it creates a gap in available housing in the coming years, which historically leads to tighter inventory and upward pressure on rents.

Recent data also shows a decline in housing permits, a key indicator of future construction activity. As permits drop, fewer new projects are entering the pipeline, reinforcing the expectation that while supply may feel elevated today, future inventory is likely to tighten, especially as builders continue to scale back development in response to current market conditions.

At the same time, the U.S. continues to face a significant housing shortage, particularly for lower-income renters. The country currently lacks 7.2 million affordable rental homes, with only 35 units available for every 100 extremely low-income renters.

This combination of short-term oversupply but long-term underbuilding is critical to understanding where the rental market is headed.

Utah Market: A Deeper Structural Housing Shortage

While national trends show temporary softening, Utah’s housing situation remains fundamentally constrained.

According to the National Low Income Housing Coalition, Utah has only 28 affordable rental homes available for every 100 extremely low-income renters, highlighting a significant supply gap. To meet current demand, the state would need at least 44,000 additional affordable units, underscoring the depth of the shortage.

This shortage is structural:

Development costs remain too high relative to affordable rent levels

Private supply is limited in lower price segments

Demand continues to outpace available housing

At the same time, affordability challenges continue to push more households into renting. With a large portion of homes out of reach for the average buyer, many residents remain renters longer, reinforcing long-term rental demand.

What’s Happening Right Now (Short-Term Reality)

Despite these long-term constraints, Utah is currently experiencing short-term pressure from a recent wave of new housing supply. Many of the units delivered over the past year are now hitting the market at the same time, temporarily increasing competition.

As a result, property owners may see:

More competition from recently delivered units

Slower leasing activity

Increased renter price sensitivity

Greater need for competitive pricing or concessions

These conditions reflect a temporary phase in the housing cycle, rather than a shift in the long-term supply-demand imbalance.

What’s Coming Next (Why This Matters for Utah)

The next phase of the market will be driven by what happens after the current wave of supply is absorbed. While recent construction has temporarily increased inventory, early indicators show that builders are beginning to slow down new development.

As fewer projects are started today, fewer units will be delivered in the coming years. In a state like Utah where a significant housing shortage already exists; this pullback is likely to tighten supply more quickly than in other markets.

This creates a likely progression:

Current excess supply gets absorbed

New construction slows

The underlying housing shortage becomes more visible again

Rental demand remains strong

Upward pressure on rents begins to return

Because Utah is already undersupplied, the impact of reduced construction may be more immediate and more pronounced, accelerating the shift back toward a more landlord-favorable market.

What This Means for Property Owners

For property owners, the market requires a balanced approach:

Short-Term Adjustments

Stay competitive with pricing

Expect longer leasing timelines

Use concessions strategically

Focus on maintaining occupancy

Long-Term Positioning

Demand remains structurally strong

Housing shortages support long-term occupancy

Slowing construction may tighten supply again

Rental properties remain positioned for long-term growth

What we’re seeing today is not a weakening market, but a transition phase within the housing cycle.

Current conditions are being shaped by a recent wave of supply entering the market, temporarily increasing competition and softening rent growth. However, Utah’s long-term fundamentals remain unchanged, driven by a persistent housing shortage and sustained rental demand. For property owners, the key is to navigate the current phase strategically while keeping a long-term perspective because Utah continues to stand out as a stable and fundamentally strong rental market over the long term.

Utah Real Estate Market

Utah’s housing market continued its upward momentum in April, building on the strong activity seen in March. The median sold price increased to $615,000, reflecting a 2.85% month-over-month gain and a 2.52% rise year over year, signaling steady price growth. Sales activity held firm at elevated levels, while inventory rose 8.51% from March, giving buyers more options in an increasingly active market. Overall, April reflects a stable and growing market, with consistent demand, rising prices, and expanding inventory helping balance conditions.

Median Sold Price* | Sold Count* | Average # of Listings* |

April: 599,900 May: 609,900 June: 615,000 July: 623,563 August: 605,000 September: 610,000 October: 600,000 November: 599,945 December: 610,000 January: 595,000 February: 588,397 March: 597,970 April: 615,000 | April: 1,431 May: 1,683 June: 1,565 July: 1,530 August: 1,604 September: 1,445 October: 1,545 November: 1,164 December: 1,397 January: 969 February: 1,246 March: 1,574 April: 1,574 | April: 5,730 May: 6,554 June: 7,042 July: 7,207 August: 7,295 September: 7,288 October: 7,208 November: 7,111 December: 5,515 January: 5,587 February: 5,554 March: 5,794 April: 6,287 |

Monthly Change: Up 2.85% | Monthly Change: 0.00% Year Over Year: Up 10.00% | Monthly Change: Up 8.51% Year Over Year: Up 9.72% |

* all graphs/data are for single-family homes in Salt Lake, Utah, and Davis Counties.

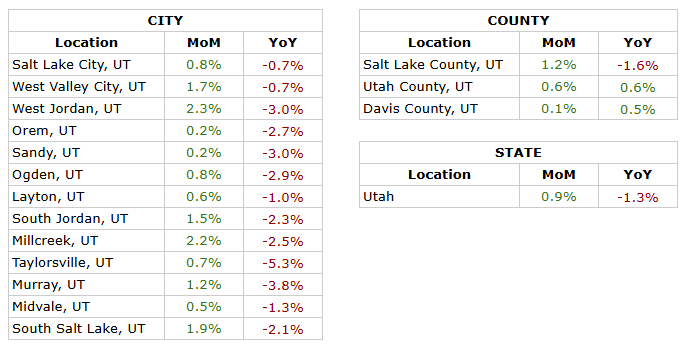

Rent Report

Utah’s rental market showed stronger upward movement in April, with statewide rents increasing 0.9% month over month while still tracking 1.3% below last year’s levels. This indicates improving short-term pricing trends as the market continues to recover year over year. At the county level, Salt Lake County recorded the highest monthly increase but remains down annually, Utah County continued to show stability with positive annual growth, and Davis County posted modest gains across both measures. City-level performance was broadly positive month over month, with most areas experiencing steady increases, while year-over-year trends remained negative across nearly all markets. Overall, April reflects a market gaining traction, with consistent monthly rent growth and early signs of strengthening demand.

*Rental data provided by apartment list.

Industry Updates

Build-to-Rent Limits May Reduce Housing Supply - Housing researchers are warning that a proposed federal policy targeting build-to-rent (BTR) housing could significantly reduce future housing supply. The provision, included in the 21st Century ROAD to Housing Act, would require BTR homes to be sold to individual homeowners within seven years, potentially making the investment model financially unworkable for developers. According to estimates from the Urban Institute, the rule could reduce annual housing construction by at least 72,000 rental units and lower both single-family and rental home completions nationwide. Industry groups argue that build-to-rent communities help serve middle-income households who may not yet be able to afford homeownership, and limiting institutional investment could worsen the country’s existing housing shortage. Researchers also noted that many BTR communities are not designed to be easily subdivided and sold individually, creating additional logistical and financial challenges.

NAA Leads FTC Rent & Fee Transparency Efforts - The National Apartment Association (NAA), along with a broad coalition of industry groups, submitted comments to the Federal Trade Commission (FTC) as part of its early-stage rulemaking process on rental fee transparency. The FTC is exploring whether new federal rules are needed to prevent unfair or deceptive fee practices in rental housing, but no final decisions have been made yet. NAA emphasized that rental housing is more complex than typical consumer transactions and warned that overly strict regulations could increase operational costs and unintentionally impact renters. Industry groups also highlighted that many states already have extensive housing regulations, and additional federal rules must account for these existing frameworks and the diversity of housing providers, including small independent owners. Moving forward, the FTC is expected to propose formal rules later this year, which could introduce nationwide standards for rent and fee transparency.

Summarize this content with AI:

Chat GPTGrok

Perplexity

Claude.ai