As summer heats up, the economy continues to send mixed signals. Inflation moved higher in May while the job market remained stronger than expected, making it increasingly likely that interest rates will remain elevated for the foreseeable future. Here in Utah, housing activity remains steady, but affordability challenges continue to make homeownership difficult for many households. In this month's update, we'll do a deep dive into what these affordability challenges mean for local rental property owners.

Headlines

May Jobs Report - The U.S. economy added 172,000 jobs in May, far exceeding expectations and demonstrating continued strength in the labor market. The unemployment rate remained at 4.3%, while wage growth stayed steady at 3.4% year over year. Hiring was strongest in leisure and hospitality, local government, healthcare, and social assistance. In addition, job gains for March and April were revised higher, indicating that employment growth has been stronger than previously reported. Overall, the labor market remains healthy, with solid hiring, stable unemployment, and steady wage growth supporting the broader economy. The strong report also reduces pressure on the Federal Reserve to lower interest rates in the near term, as the job market continues to show resilience despite ongoing inflation concerns.

Weekly Jobless Claims - U.S. jobless claims increased slightly last week, with 229,000 Americans filing for unemployment benefits, suggesting the labor market remains resilient despite signs of slower hiring. The national unemployment rate held steady at 4.3%, supported by continued job growth and relatively low layoffs. In Utah, initial unemployment claims rose to 1,400, up from 1,090 the previous week, an increase of 310 claims. While this represents a noticeable week-over-week increase, Utah's labor market remains relatively healthy and continues to reflect the broader national trend of low layoffs but more cautious hiring. Overall, employment conditions remain stable, though there are growing signs that finding a new job may be becoming more challenging than it was earlier in the year.

Consumer Price Index - Consumer inflation accelerated in May, with the Consumer Price Index (CPI) rising 4.2% year over year, marking the highest level in three years. Much of the increase was driven by a sharp rise in energy prices, which climbed 23.5% annually, while core inflation which excludes food and energy remained more moderate at 2.9%. Consumers continued to face higher costs for essentials such as gas, food, electricity, housing, and medical care. Despite the inflation increase, underlying price pressures showed signs of stability, as shelter costs grew at a slower pace and core goods prices declined slightly. The report reinforces expectations that the Federal Reserve will likely keep interest rates unchanged at its June meeting while continuing to monitor inflation trends and energy market developments.

Fed Meeting - Since the Federal Reserve's next meeting is scheduled for June 16–17, we are unable to cover the outcome in this month's publication. We will provide a full update on the meeting, including any policy changes and market implications, in next month's report. At its most recent meeting, the Federal Reserve held its benchmark interest rate steady at 3.50%–3.75%, reflecting a cautious approach as officials continue to balance inflation concerns with a stable labor market. While inflation has moderated from previous highs, it remains above the Fed's long-term target, leading policymakers to keep rates unchanged for now. Recent economic data, including stronger-than-expected job growth in May and steady unemployment, has reinforced expectations that the Fed will likely leave rates unchanged again at the June meeting.

The Growing Cost of Homeownership Continues to Support Rental Demand

For years, one of the biggest questions facing rental property owners has been whether renters will eventually leave the market and become homeowners. Today, that transition is becoming increasingly difficult.

A recent study by Apartment List highlights just how much the economics of housing have changed. In 2024, the median monthly cost of homeownership climbed to $2,679, compared to $1,630 for renting. That means the typical new homeowner now spends approximately 64% more per month than the typical renter. The gap has widened significantly in recent years as home prices, mortgage rates, insurance premiums, and property taxes have risen faster than rents.

As a result, many households that may have purchased a home just a few years ago are delaying that decision and remaining renters for longer periods.

Why This Matters Even More in Utah

While affordability challenges are affecting much of the country, Utah faces additional pressures that make this trend particularly significant.

Research from the Kem C. Gardner Policy Institute shows that home prices in Utah have increased substantially faster than incomes over the past decade. Combined with elevated mortgage rates, the cost of entering the housing market remains a major challenge for many prospective buyers. At the same time, Utah continues to face a long-term housing shortage. According to the National Low Income Housing Coalition, the state currently has only 28 affordable and available rental homes for every 100 extremely low-income renters and needs approximately 44,000 additional affordable housing units to meet existing demand.

These conditions limit the ability of many households to transition into homeownership, keeping demand for rental housing stronger than it might otherwise be.

What This Means for Rental Owners

For property owners, these trends help explain why rental demand has remained resilient despite changing market conditions. While recent supply additions have increased competition in some areas, the underlying demand drivers remain strong. Many households still aspire to own a home, but the financial barriers are significantly higher than they were just a few years ago.

As long as home prices remain elevated, mortgage rates stay above historical averages, and affordability challenges persist, many Utah residents will continue to rent longer than previous generations. This creates a larger and more stable renter pool, helping support long-term occupancy across the rental market.

Looking Ahead

Market conditions will continue to fluctuate, but the growing gap between renting and buying is becoming one of the most important long-term trends shaping housing demand.

For rental property owners, the message is clear: while short-term market cycles may create periods of increased competition (as we are seeing now), the fundamental drivers of rental demand remain firmly in place. Until homeownership becomes meaningfully more affordable, rental housing will continue to both play a critical role in meeting Utah's housing needs and provide attractive investment opportunities for rental property operators.

Utah Real Estate Market

Utah’s housing market maintained its positive momentum in May, supported by rising sales activity and a notable increase in available inventory. The median sold price edged up to $615,230, reflecting stable home values with a 0.04% increase from April and a 0.87% gain year over year. Home sales strengthened during the month, increasing 7.69% from April, while active listings climbed 11.83%, providing buyers with more options than in recent months. Overall, May points to a healthy and balanced market, where growing inventory is helping keep pace with demand while prices continue to hold steady.

Median Sold Price* | Sold Count* | Average # of Listings* |

May: 609,900 June: 615,000 July: 623,563 August: 605,000 September: 610,000 October: 600,000 November: 599,945 December: 610,000 January: 595,000 February: 588,397 March: 597,970 April: 615,000 May: 615,230 | May: 1,683 June: 1,565 July: 1,530 August: 1,604 September: 1,445 October: 1,545 November: 1,164 December: 1,397 January: 969 February: 1,246 March: 1,574 April: 1,574 May: 1,695 | May: 6,554 June: 7,042 July: 7,207 August: 7,295 September: 7,288 October: 7,208 November: 7,111 December: 5,515 January: 5,587 February: 5,554 March: 5,794 April: 6,287 May: 7,031 |

Monthly Change: Up 0.04% | Monthly Change: 7.69% Year Over Year: Up 0.71% | Monthly Change: Up 11.83% Year Over Year: Up 7.28% |

* all graphs/data are for single-family homes in Salt Lake, Utah, and Davis Counties.

Rent Report

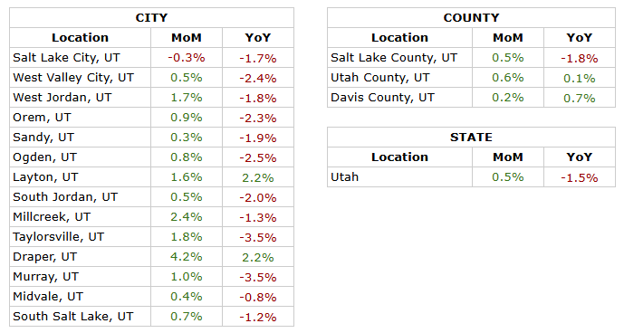

Utah’s rental market continued to see moderate rent growth in May, with statewide rents increasing 0.5% month over month, though remaining 1.5% below levels recorded a year ago. The positive monthly increase reflects continued stability in rental pricing as the market gradually works through year-over-year softness. At the county level, all major counties posted monthly gains, led by Utah County at 0.6%, which also remained slightly positive year over year. Davis County continued to show stability with positive growth on both measures, while Salt Lake County remained below last year’s levels despite monthly improvement. City-level performance was largely positive month over month, with Millcreek and Draper recording the strongest gains. However, most cities continued to report lower rents compared to a year ago, with Draper and Layton standing out as notable exceptions. Overall, May reflects a rental market that remains stable, with steady monthly increases helping offset ongoing year-over-year softness across much of the state.

*Rental data provided by apartment list.

Industry Updates

Apartment Market Pulse Q1 2026 - The U.S. economy remained resilient in the first quarter of 2026 despite slower growth, persistent inflation, and rising geopolitical tensions. The Federal Reserve kept interest rates unchanged as inflation remained above target, while mortgage rates climbed back to around 6.5%. The labor market stayed relatively stable, with unemployment holding at 4.3%, though hiring activity continued to show signs of slowing. In the apartment sector, demand moderated while new supply remained elevated, creating a more balanced market environment. Despite these challenges, national occupancy remained healthy and rent growth stayed positive overall. Looking ahead, slowing construction activity may help support market stability as existing supply is absorbed.

Housing Supply Takes Center Stage in New Federal Legislation - The U.S. House passed an amended version of the 21st Century ROAD to Housing Act, a bipartisan housing bill focused on increasing housing supply and improving affordability. The revised legislation includes measures to streamline housing development, reduce regulatory barriers, modernize federal housing programs, and encourage new construction. A key change was the removal of a controversial provision that would have restricted build-to-rent (BTR) communities, helping preserve an important source of rental housing. Supporters believe the bill could help address housing shortages, ease affordability challenges, and create more pathways to both renting and homeownership. The bill now returns to the Senate for further consideration before it can be signed into law.

Summarize this content with AI:

Chat GPTGrok

Perplexity

Claude.ai